Smartphone reviews, tips, news, guides, and updates for Android & iPhone.

India’s Smartphone Market: Explosive Growth, Premium Push & User Realities

The Indian smartphone market is a juggernaut, not just in terms of the sheer number of devices sold, but in its rapid evolution from a budget-first to an aspirations-driven ecosystem. It’s a landscape where value is aggressively chasing volume, fundamentally reshaping what consumers expect and what brands must deliver. With projections suggesting a market value surpassing $50 billion by 2025, the story is no longer just about getting a phone; it’s about getting the right phone.

In a Nutshell

- The Premium Shift: While overall shipment volumes remain massive, the real story is the surge in value. The average selling price (ASP) for smartphones hit a record $282 in 2025, an 8% year-over-year increase, fueled by relentless demand for premium models.

- 5G is the New Normal: 5G devices now represent the vast majority of smartphone shipments, with penetration hitting 79% in 2024. This rapid adoption is driven by expanding network coverage and a flood of affordable 5G handsets.

- Financing is the Fuel: The entire premium push is largely bankrolled by accessible credit. No-Cost EMIs and zero down payment schemes have democratized aspirational purchases, making higher-priced devices a reality for millions.

Decoding Market Size: More Than Just Numbers

The Indian smartphone market is a complex beast, with its size best understood through two lenses: volume (units shipped) and value (total revenue). While shipment volumes saw marginal growth to 152 million units in 2025, the market’s total value jumped a staggering 9% in 2024, hitting an all-time high, a trend that continued with 8% value growth in 2025. This tells us one thing loud and clear: Indians are spending more per phone than ever before.

Observing the quarterly reports, it’s clear the market’s centre of gravity is shifting from units sold to revenue generated. This phenomenon, often termed ‘premiumization,’ is seeing consumers leapfrog from entry-level devices to mid-range and even premium flagships. The premium segment (phones over ₹30,000) is the fastest-growing category, now accounting for 22% of total shipments. Why this sudden urge to splurge? A combination of higher disposable incomes, the desire for better features like superior cameras and processing power, and, most critically, the widespread availability of easy financing options.

Rise of 5G: From Luxury to Ubiquity

5G is no longer a feature reserved for the elite. 5G-enabled smartphones accounted for a whopping 79% of shipments in 2024, and this figure is only set to grow. By the end of 2025, India is projected to have 394 million 5G subscriptions, a number expected to cross the 1 billion mark by 2031. The rollout has been aggressive, with 5G services available in 99.6% of districts as of early 2025.

This rapid adoption is a two-way street. Telecom operators are expanding their networks at a breakneck pace, and manufacturers are flooding the market with affordable 5G handsets. In fact, the sub-₹10,000 5G segment has seen explosive growth. However, this has its own set of teething problems, as one user points out, “5G is fast, but it’s not available everywhere yet. And it drains the battery like crazy.” This highlights a gap between network availability and the hardware’s ability to cope efficiently, a challenge brands must address in their quest for better smartphone battery performance.

‘Make in India’ Paradox: Assembly Hub, Not Component King

The ‘Make in India’ initiative has been transformative, turning India into the world’s second-largest mobile phone manufacturer. An incredible 99.2% of all smartphones sold in the country are now locally assembled, a massive leap from just 26% in 2014-15. This has been driven by government schemes like the Production-Linked Incentive (PLI), which encourages global giants to set up shop here.

However, there’s a catch. As one user shrewdly observes, “The ‘Made in India’ tag doesn’t mean much to me if the quality isn’t there. Most of the parts are still from China anyway.” This sentiment reflects the underlying reality: India excels at assembly, but still heavily relies on imported components like chipsets and display panels. While progress is being made in local value addition, which has grown to 20%, the journey towards true self-reliance is a long one.

Ground Realities: What Users Truly Feel

High-level market data tells only half the story. The lived experience of the Indian smartphone user is a mixed bag of satisfaction and frustration.

Value is Everything

“Value for money is a huge factor for me. I’d rather get a phone with 90% of the flagship features for 50% of the price.” This user opinion perfectly captures the market’s core philosophy. Brands like Vivo, Xiaomi, and Samsung dominate by offering feature-packed devices at competitive price points. Even as they spend more, Indian consumers are incredibly discerning, weighing every rupee against the performance and features offered. This is why a device like the IQ 15R can cause such a stir.

After-Sales Service and Software Experience

Two of the most significant pain points for users are after-sales service and the software experience. “After-sales service is a lottery in India,” laments one user. Another complains, “I’m tired of all the bloatware and ads on my phone. I wish manufacturers would offer a cleaner Android experience.” These issues, particularly the pre-installed apps and ads that subsidize the cost of budget phones, are a constant source of annoyance and represent a key area where brands can differentiate themselves.

The Financing Engine: No-Cost EMI

“Getting a good phone on EMI without any extra cost is a game-changer. It’s the only way I could afford my current phone.” This statement underlines the monumental role of financial products in the market’s growth. No-Cost EMI has made premium devices like the latest Samsung Galaxy S26 Ultra accessible to a much broader audience, effectively lowering the barrier to entry for the premium segment. While not always truly “no-cost” due to waived discounts or processing fees, they are a powerful tool for driving sales.

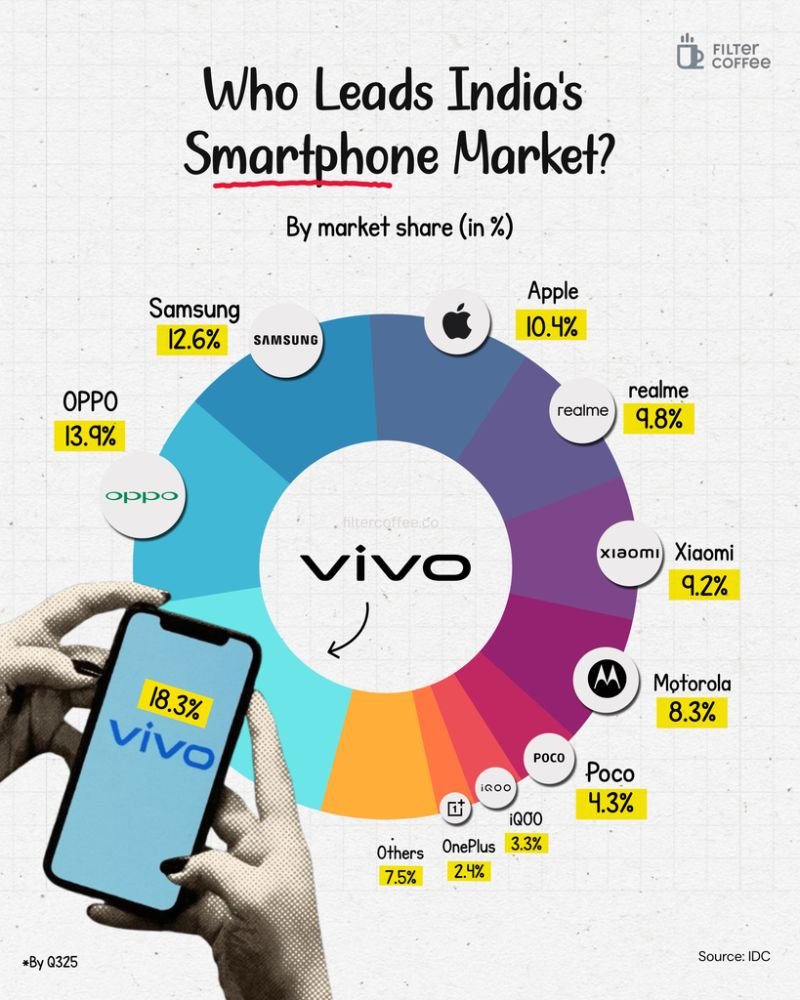

Competitive Landscape: A Fierce Battleground

The fight for market share in India is intense. Vivo currently leads the pack in terms of shipment volume, closely followed by major players like Xiaomi and Samsung. However, the premium space tells a different story. Apple, despite a smaller volume share, leads the market significantly in terms of value. The iPhone has become a status symbol, and its growing shipments have made India Apple’s fourth-largest market globally.

Underneath the brand wars is a battle of components. The chipset market is largely a duel between MediaTek, which holds the majority share, and Qualcomm. Their processors power nearly every device, and their competition directly influences the price and performance that consumers ultimately experience.

Conclusion: What’s Next for India’s Smartphone Market?

India’s smartphone market is at a fascinating crossroads. The explosive growth in value, driven by the ‘premiumization’ trend and fueled by accessible financing, shows a market that is maturing rapidly. At the same time, it remains incredibly price-sensitive, with users demanding maximum value and a clean, reliable experience for their money. The future will likely see an even more intense focus on the premium segment, the continued decline of feature phones, and a greater push for local component manufacturing to add more substance to the ‘Make in India’ story. For the millions of users across the country, this competition can only mean one thing: more choice, better features, and even more value.